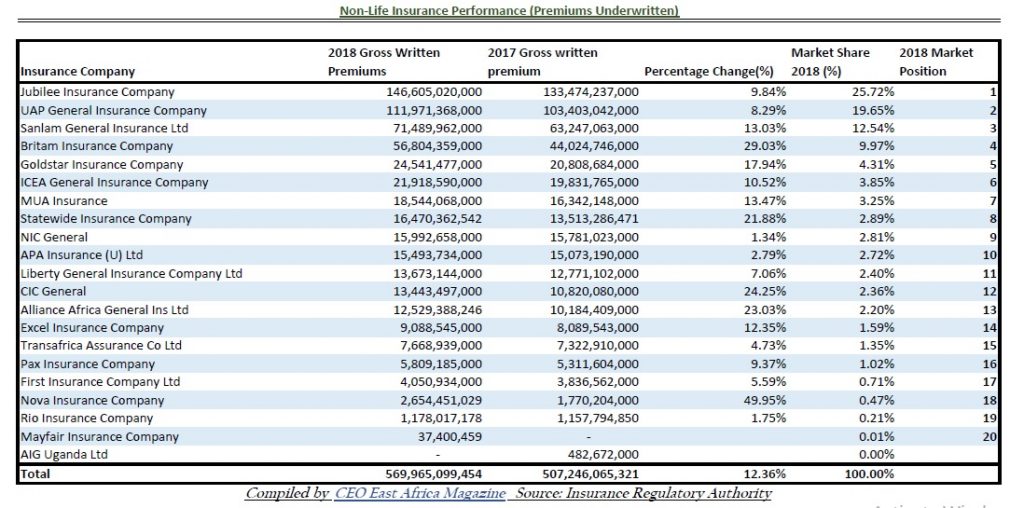

The top 10 non-life insurance companies, control 87.7% of the category, having underwritten UGX499.8 billion in premiums- out of a total of UGX569.96bn in non-life category premiums.

They are: Jubilee Insurance, UAP General Insurance, Sanlam General Insurance, Britam Insurance, Goldstar Insurance, ICEA General Insurance, MUA Insurance, Statewide Insurance, NIC General and APA Insurance in that order.

The top 10 non-life players grew their premiums by 12.2%, lower than the industry average growth- as life insurance continued to eat into non-life insurance.

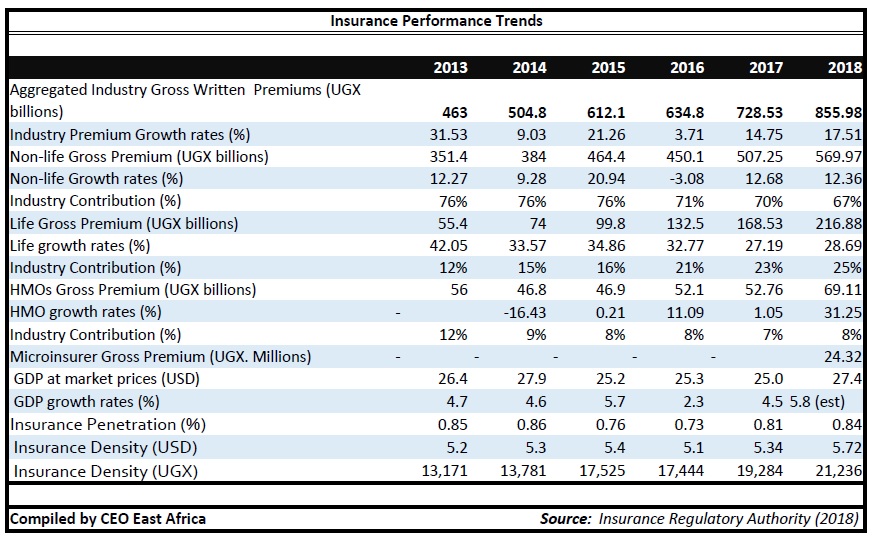

According to the Insurance Regulatory Authority, non-life insurance accounted for UGX570 billion (66.6%), while life accounted for UGX216.9 billion (25.3%) and Health Membership Organisations (HMO’s) Shs69.1bn (8.1%). Dedicated micro insurance organizations underwrote Shs24.31 million.

Life and HMOs grew faster than the industry at 28.7% and 31.3% respectively. The entire industry grew by 17.5% while non-life business grew by 12.36%

Two (2) companies underwrote premiums in excess of UGX100bn while nine (9) companies underwrote between UGX10 billion to UGX50 billion. Six (6) companies underwrote premiums below UGX10bn while one company underwrote UGX1 billion.

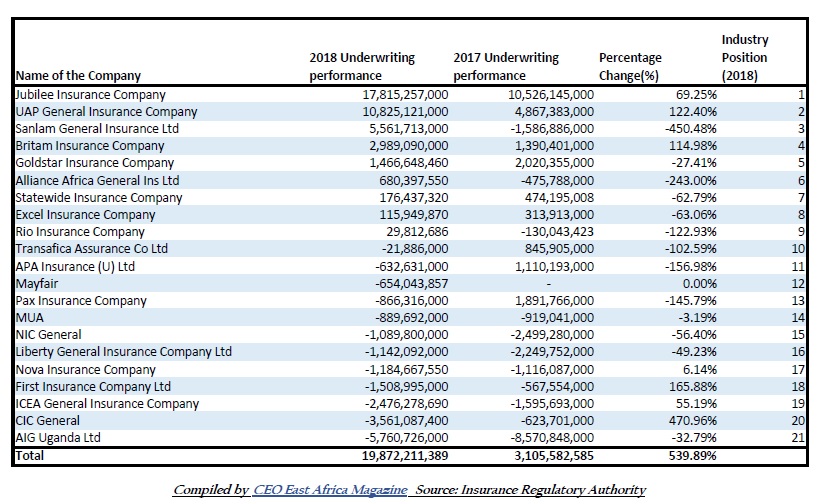

Nine (9) companies made underwriting profits while 12 companies made underwriting losses. Total industry profitability stood at UGX39.7 billion while losses stood at UGX19.8 billion.

Top-heavy industry

The biggest chunk of the top 10, is controlled by the largest 5 insurance companies, who in between them control 71.95% of the market (UGX411.4 billion) – a growth of 12.73%. Like in the banking industry which is also top heavy, the industry is largely dominated by the top 3 players- Jubilee, UAP and Sanlam who in between them control nearly 60% of the entire market.

The top 10 non-life insurance companies, control 87.7% of the category, having underwritten UGX499.8 billion in premiums- out of a total of UGX569.96bn in non-life category premiums. Two (2) companies underwrote premiums in excess of UGX100bn while nine (9) companies underwrote between UGX10 billion to UGX50 billion. Six (6) companies underwrote premiums below UGX10bn while one company underwrote UGX1 billion.

Such is the disparity that, Jubilee Insurance, the No.1 player- UGX146.6 billion in 2018 premiums, is bigger than the 15 insurance companies from the bottom of the table combined. The 14 companies, some of whom have been around for over a decade, together underwrote UGX136.6 billion in premiums.

The fastest growing company among the top 10 was Britam Insurance which grew written premiums by 29% from UGX44 billion in 2017 to UGX56.8 billion. Fast-growing Britam Insurance in 2017 briefly held the 3rd position, having overtaken Lion Assurance to occupy the position held by AIG Insurance which exited the market.

But following the November 2017 acquisition cum merger of fourth-placed Lion Assurance Company and fifth-placed Sanlam Insurance, created a stronger No.3 Sanlam.

AIG has since re-entered the market as a Greenfield operation.

The top 10 in numbers and profits

The Aga Khan owned Jubilee Insurance maintained its top position, growing premiums by 9.8% from UGX133.47bn to UGX 146.6 billion. Jubilee Insurance, also remained the most profitable insurance firm, increasing their underwriting profit by 69.25% from UGX10.5 billion in 2017 to UGX17.8 billion- accounting for 44.9% of the UGX39.66 billion profits, made by the 9 profitable firms.

Airtel Africa and SpaceX Announce Strategic Partnership to Launch Starlink Direct to Cell Connectivity Across Africa

Airtel Africa and SpaceX Announce Strategic Partnership to Launch Starlink Direct to Cell Connectivity Across Africa

UAP General Insurance was the 2nd biggest in premiums underwritten at UGX111.97 billion, up 8.29% from UGX103.4 billion in 2017. UAP was also the second most profitable, general insurance firm, increasing their net revenue by 122.4% from UGX4.86bn in 2017 to UGX10.82 billion.

UAP & Jubilee were the only 2 firms that underwrote premiums above UGX100 billion in 2017 and 2018.

Sanlam in the 3rd position with UGX 71.48 billion in premiums, also recovered from a UGX1.58 billion loss in 2017, to post a profit of UGX5.56 billion, becoming the 3rd most profitable firm in 2018 as well.

Britam Insurance, in the 4th position with UGX56.8 billion premiums was also the 4th most profitable firm, having increased their underwriting profit by 114.98%, from UGX1.39 billion to UGX2.98 billion.

Goldstar Insurance in the 5th position, underwrote UGX24.54 billion; their profit slightly reduced from UGX2 billion to UGX1.46 billion but remained the 5th most profitable insurance firm in 2018.

ICEA in the 6th position underwrote UGX21.91 billion, MUA Insurance in the 7th position underwrote UGX18.54 billion while Statewide Insurance in the 8th position, underwrote UGX16.47 billion.

NIC General in the 9th position underwrote UGX15.99 billion while APA Insurance in the 10th position, underwrote UGX15.49 billion.

Four (4) of the top 10 companies by premiums, made losses. They are ICEA General Insurance whose loss position widened from UGX1.59 billion in 2017 to UGX2.47 billion, MUA Insurance who posted a UGX889.69 million loss, NIC General who narrowed their losses from UGX2.49 billion in 2018 to UGX1.08 billion and APA Insurance who went from a UGX1.11 billion profit in 2017 to a UGX632 million loss.

Four (4) firms that are not in the top 10, but were profitable, include: Alliance Africa General Insurance that posted a UGX680.39 million, Statewide Insurance which posted UGX176.43 million profit, Excel Insurance that posted UGX115.94 million in profits and Rio Insurance, UGX29.81 million in profits.

Agricultural insurance struggles to grow

A total of UGX 5.24bn was underwritten in 2018 under the Uganda Agricultural Insurance Scheme (UAIS) compared to UGX 5.20bn in 2017.

This was against the sum insured of UGX 387bn in 2018 and UGX 235.7bn in 2017.

UAIS) a Public Private Partnership (PPP) arrangement with Uganda Insurers Association (UIA), the Government of Uganda that subsidises premiums for farmers for a five (5) year period starting in FY 2016/17.

Total Claims paid amounted to UGX 2bn (with Poultry accounting for over 67.3%) compared to UGX 1.9bn and multi-peril crop insurance accounting for 84%) in 2017 claims. The scheme has grown coverage from about 5,000 farmers in 2015/16 to an expected coverage of 100,000 farmers by the end of FY 2018/19.