Stanbic Bank, Uganda’s largest bank by assets, lending, deposits and profits, today released their H1 2019 results, signaling what should turn out to be yet another strong year.

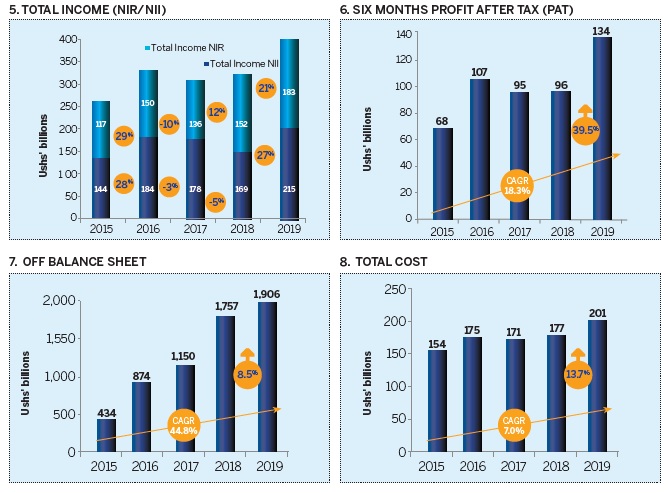

In results announced today, the bank which has gone aggressively digital, executing 85% of their transactional volumes through their branchless platforms- including 20% of this on agent banking alone, picked up UGX550 billion in new deposits and lent out more UGX400 billion than it did in H1 2018, announced that net profit had grown 39.5% from UGX 96.1 billion in June 2018 to UGX 134.1 billion at the end of June 2019- net H1 2018 profits only grew by 1%.

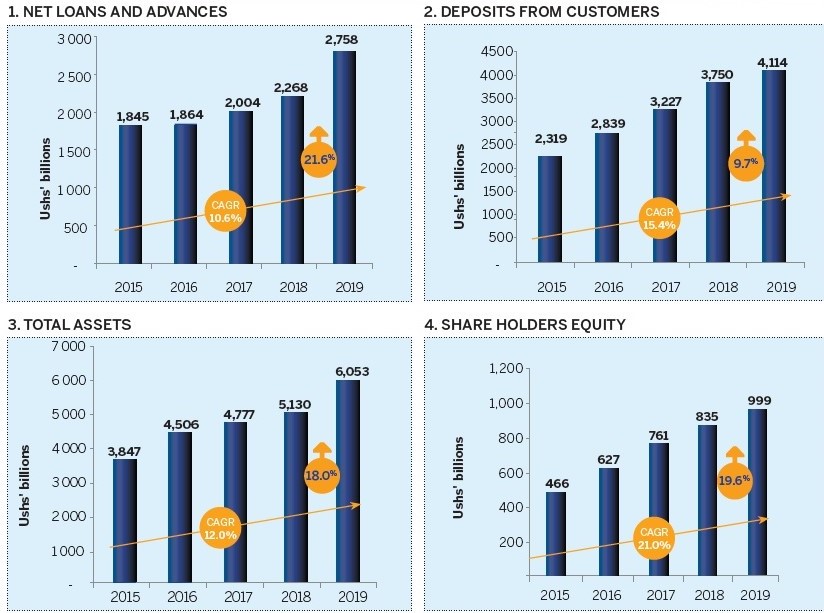

The bank added a fresh UGX1 trillion on their asset book- reaching a historical UGX 6.1 trillion in assets!

In this interview adopted from their results announcement, Patrick Mweheire, the bank’s Chief Executive Officer, talks about the bank’s results against the backdrop of a rebounding economy, the bank’s investment in technology and SMEs, all of which he says, point to an even greater full 2019.

What’s Your Current Assessment of the Ugandan Economy?

The economy remains relatively strong with robust growth across many sectors. GDP growth was a positive 6.0% in fiscal 2018 which confirms that we have really turned the corner with even more positive momentum poised for 2019. Private sector credit growth has also bounced back – averaging 14% in the first half of 2019.

We are seeing a rebound in the key manufacturing, construction and agriculture sectors. Personal borrowing and trade also continue to grow; which is a very positive development for the country. Inflation remains below the 5% area so we expect the Central Bank to maintain their monetary stance and not pass an increase in the Central Bank Rate (“CBR”) in 2019.

This will ultimately keep interest rates or prime lending rates where they are. Notwithstanding this positive local environment, we have to be cognizant of the global headwinds such as Brexit or the China-US Trade wars and how they will ultimately crystallise back into the East African region.

How would you describe your half-year performance and what were the key drivers contributing to your performance?

We’ve had a remarkable performance over the past six months underpinned by our customer centric approach and the strength of our diversified businesses. Our Profits after Tax grew almost 40% year-on-year from UGX 96.1 billion in June 2018 to UGX 134.1 billion at the end of June 2019; Customer deposits grew approximately 10% to exceed UGX 4.1 trillion up from UGX 3.75 trillion in June 2018.

We continued to extend the most new credit in the sector – approximately UGX 400 billion in new credit – which grew our loan portfolio by 21.6% to UGX 2.7 trillion from UGX 2.3 trillion in June 2018. The growth has been largely due to improved economic activity as credit growth across all customer segments improved. We remain a key enabler in major sectors such as agriculture, manufacturing, construction and trade sectors especially supporting the SME sector.

The bank’s total assets also grew 18% and crossed UGX 6.1 trillion from UGX 5.1 trillion putting us in a much stronger position to support larger development projects and better facilitate economic growth in the country. This strong asset growth was accentuated by strong customer deposit growth with excess liquidity being appropriately deployed across the different asset classes, mainly customer loans, government securities and interbank lending.

The bank has been aggressively pursuing a digital strategy- what have been the dividends to date- especially over the past 6 months?

I am quite pleased on the progress so far. Branch transactions now account for less than 15% of our total transactional volumes which means we are executing 85% of our transactions on our digital channels which includes Agency banking.

This is significant for two key reasons – it enhances the customer experience by providing a 24/7 digital platform for customers to execute their day-to-day banking wherever and whenever they want. It also reduces the cost of doing business and enhances efficiency as it is of no value queuing in branches to execute low value transactions such as paying utilities or school fees.

We also successfully launched our online account opening platform which allows new customers to open personal accounts digitally. It offers a convenient and seamless on-boarding that demonstrates our commitment to digitization and innovation. This allows customers to literally on-board themselves as bank customers on the go – any time and anywhere across the country.

It’s worthwhile touching on Agent Banking as well. With 1,000 active agents across the country, it has greatly increased our customer touch points and provided choice to our customers in executing their day to day financial transactions. This new channel (less than a year old) now represents 20% of all our transactional volumes today. Our customers can now access a wide range of services including cash deposits and withdrawals, bill payments, school fees collections, fund transfers and a number of other new features yet to be introduced. It gives us an opportunity to de-clutter the branches and offer a better customer experience for the more high value and high touch transactions.

In the past years we have witnessed heightened focus by Stanbic on SMEs; how significant is this segment to the bank?

SME’s are the key engine of growth for our economy and employ an excess of 2.5 million people, significantly higher than the corporate private sector at approximately 800,000. You simply cannot grow Uganda without growing the SME’s. It’s really that simple; which is why we established a Business Incubator that provides capacity development programmes for entrepreneurs in SME’s. It trains and provides them with soft and hard skills necessary to improve their business operations and compete more effectively in the market place.

It also deliberately prepares them to leverage the upcoming opportunities in Uganda’s emerging Oil & Gas sector.

Over the last 18 months, the incubator has run three successful cohorts and a total of 1,062 entrepreneurs from 300 SME’s have been successfully trained and graduated from the incubator. I am happy to report that in the next few weeks, we shall be launching regional incubator centres in Mbarara, Mbale and Gulu in order to avail similar training and development opportunities to SME’s in the rural areas.

We do this at absolutely no cost to the SME’s and more importantly – you do not have to be a Stanbic client to apply and participate.

Looking ahead, what is the key focus for the bank over the next half of the year?

The priority for us remains ensuring that our clients’ needs are appropriately and effectively met. We continue to focus on strengthening our propositions by providing solutions that meet our clients’ needs and help them achieve their aspirations. We believe that focusing on the client is the reason for our robust double-digit balance sheet growth across deposits, loans and trade and ultimately the reason for our client revenue growth of ~11% in the first half of the year.

We will continue this focus into the second half of the year through customizing services, focusing on meeting client service level agreements, delivering client journeys and transforming the bank into an organization that is future ready.